Previously in our Blog, we have explored the need for corporate purpose and to ask the question “why” companies do what they do. We emphasized the significance of an inspiring purpose articulated in the form of a mission statement in ensuring durable, high quality relationships with stakeholders.

Many companies, especially in Europe, have moved on from this to ask themselves an even harder question; “why not?” Either because of regulation or because of increasing pressure from investors, customers, and other stakeholders, the conversation is now much more about explaining why you are not incorporating ESG metrics into your business rather than why you should be doing so.

Looking at financial markets especially in the covid19 era, one of the trends which has stood out starkly is the continuing stock market outperformance of a narrow set of corporates. Many of these are beneficiaries of the work-from-home trend are concentrated in the technology or pharmaceutical sectors. However, there are other companies which are not such obvious beneficiaries of the pandemic and yet are linked by a common thread; all of them derive a significant portion of their value from intangible assets. Consequently, market participants are questioning the validity of traditional investment tools and techniques. Part of the reason for this seeming anomaly is that measurements like book value may not be accurately capturing a company’s intangible assets; such as the strength of their brand or the value of their intellectual property and their social capital.

What then are these intangible assets and how should corporates think about them if they are indeed driving market value?

Assets are everything a company owns. Tangible assets are physical. Intangible assets do not exist in physical form. They may include things like patents and goodwill which are more measurable but also less easily quantifiable and non-physical assets such as customer satisfaction, resources and networks built by capable employees. Moats which money cannot buy and which take time and a proper culture and climate to build. This is one main reason why many mergers and acquisitions do not create the anticipated post-deal value; post-merger integration of these intangibles is often not successful due to a cultural misalignment between the acquirer and the acquired.

What we mean by intangible assets has evolved rapidly over the last two decades. Historically, intangibles mainly consisted of goodwill which emerged primarily via acquisition accounting conventions. However today, as we have argued here, intangible value is much more varied and complex making it harder to value and requiring a company by company analysis.

Let us look at the consumer sector where the market is ready to pay high multiples for companies owning strong brands. Investors take comfort from a brand that keeps customers coming back for repeat purchases and so helps generate profits over a longer than usual time period. But the value of these brands is not easy to capture and reflect in a balance sheet using conventional accounting metrics. How do you value a customer’s sense of trust and security? How do you value the premium that this allows the owner of a well-regarded brand to charge? The value can, in part, be gauged when we look at brands which have gone through negative PR events. For example, Tylenol recovered fast from a poisoning scandal in the 1980s due to strong customer trust in the brand. Or, Coca-Cola which rebounded from a PR disaster in 1999, when it began testing vending machines that automatically raised prices during the summer heat and consequently was accused of “price gouging” and taking advantage of customers exactly when they had the maximum need for the product.

A key contributor to the generation of intangible value is human capital1. Broadly speaking, there are two main components to human capital, internal and external. Internal consists of your employees; their ability to create new products, resources or client relationships can often be the most crucial factor to determine the success or failure of an enterprise. External consists of your customers and business partners such as suppliers and dealers, who not only provide a monetizable asset but also, hopefully bestow upon a corporation both a positive reputation and a strong brand. Reputation and brand can be lost in a heartbeat if trust in the corporation is broken as some social media platforms are discovering.

The position of employees has dramatically changed over time. Corporations that start their actions with the even tougher question of “why not” than “why” and who pay more than lip service to the ESG concepts they avow view their workforce as an organizational asset and not just an expense line in their financial statements. To maximize the value of this intangible asset, especially in those companies (technology focused for instance) that possess a relatively youthful workforce, corporate values and employee values need to be aligned. This will involve a focus on many of the issues underpinning the ESG conversation. To value the intangible asset represented by a company’s human resources correctly, it is essential to assess the quality of a company’s commitment to its ESG principles and whether or not corporate talk is being effectively and genuinely put into practice.

Incomplete and insufficient reporting of intangible assets leads to a host of problems for analysts, investors, boards, and stakeholders. Poor information on intangible assets means that analysts’ valuations may not be accurate. This, in turn, has negative effects on share price volatility, affecting the ability of a business to secure fairly priced funding. Equally, when the true value of assets is missing, boards and shareholders are disposed to selling assets below reasonable prices and possibly ignoring some business risks that face the enterprise.

As a consequence of the increasing importance of intangible assets, there is a developing disconnect between the valuations assessed by financial markets and the valuations assessed by the accounting (book) value of many enterprises. Accounting statements often do not capture the value represented by intangibles – for example traditional metrics of valuation show some technology companies as overvalued on accounting-based balance sheets that mostly reflect physical assets. Markets are often more insightful and better integrate the future potential of intangibles in their valuations. Hence, the current market debate between the supporters of value and those of growth. An argument that is currently being won hands down by growth investors.

Two stock exchanges Australian Stock Exchange and Nasdaq, provide perfect examples of this trend. Net tangible assets represent only 37 per cent of the enterprise value of the ASX 200. Nasdaq is even further along the asset evolution curve with only five per cent of value attributed to net tangible assets. On both exchanges, only a small proportion of value is explained by those intangible assets on company balance sheets. Approximately 15 per cent of the valuation in the financial statements of these companies are intangibles in each market. This is a function of restrictions placed by accounting standards on capitalizing internally generated intangible assets, and as a result, a substantial portion of enterprise value is not explained by balance sheets (48 per cent of the ASX and 75 per cent of Nasdaq).2

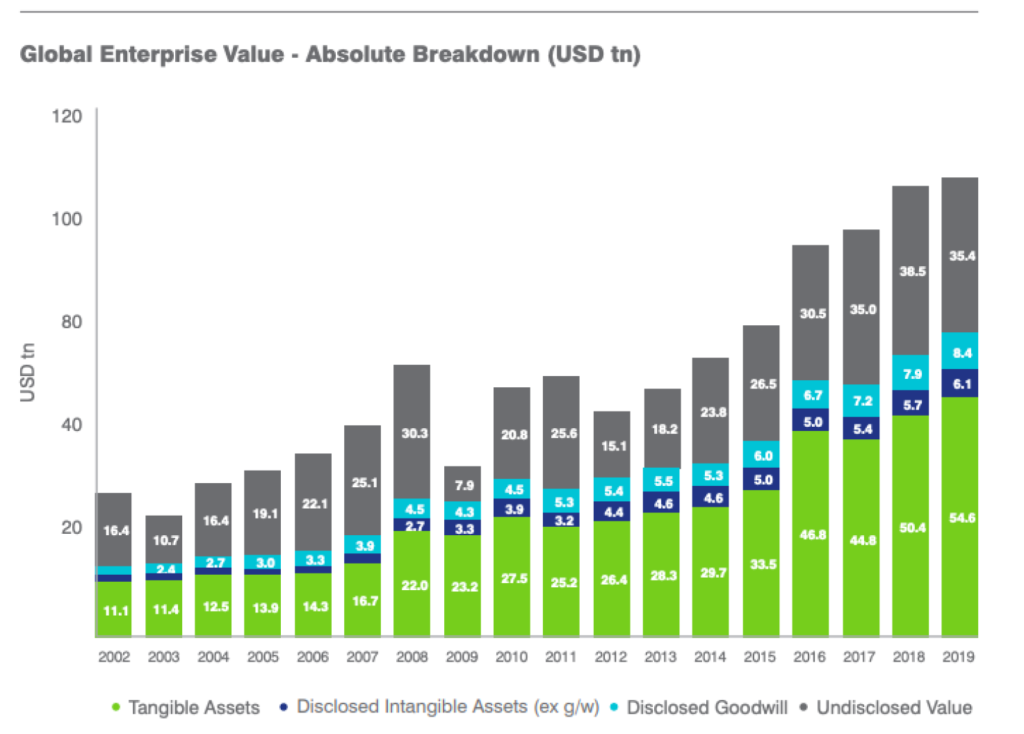

Indeed traditional financial accounting is unable to keep up with these new types of assets. “What is the solution? Can we pretend these assets don’t exist just because accounting conventions are unable to capture them?” is a question Paul Chan – President of Malaysian Alliance of Directors – asks in his article called “Governance 4.0 Redefining & Reinventing Governance”3. Markets seem in no doubt about their importance. The current value of the world’s undisclosed intangible assets is now at US$35.4 trillion which is around 35% of global enterprise value that stands today at US$104.5 trillion according to Global Intangible Finance Tracker (GIFT) report.4

Lots of corporations in sectors which are human capital dependent such as Google and Facebook go out of the way to provide employee amenities like flexible working, canteens, sports facilities, onsite launderettes, “dogs are welcome” policy, shuttle busses, free onsite haircuts, discounts for events, 7 weeks paternity leave, massage therapists, and onsite medical stuff etc. simply to remain competitive in getting access to the best employees. To underinvest in their human capital in client acquisition is to fail to properly manage risks to brand and reputation and/or to build intellectual property.

When we look at the ESG world, corporates are increasingly facing the same challenges that are apparent in the struggle to properly value intangibles. Companies recognize that a long-term commitment to ESG Principles is necessary for long term value creation and that many investors care passionately about ESG. But how does a company capture the value of this commitment to ESG on its balance sheet? Current traditional accounting regulations do not provide a good template to report ESG activities. Investors struggle to find the information necessary to evaluate a company’s commitment to ESG within the report and accounts. Two core elements are missing in order to correct for this.Firstly, a universal consensus on what constitutes an ESG investment; and secondly, agreed, standardized reporting which would help both measurability and comparability.

Again, asking the more difficult question “why not” rather than “why” may help resolve both issues. Unquestionably, there are major accounting challenges for corporations in integrating intangible assets into their balance sheets. These will include the objective measurement of the value of human capital, reputation, brands, and customers as the scope for misstatement and poor ethical practices in these areas will be large.

These are not easy issues to resolve and challenges are real. In addition to consistency of leadership at management and board level, holistic thinking as well as the integrated reporting framework may be providing some answers. New developments in management, including the new EFQM Model 2020 and Integrated Reporting are trying to address these issues.

The logic of the new EFQM model (Why-Direction, How-Execution, What-Results) is fundamental as it addresses not only how to be excellent but also, more importantly, how to be radically different; through understanding and reacting to all the relevant megatrends and influences in the environment. At the same time the Model focuses on measuring inputs, outputs and outcomes from different perspectives, thereby helping institutions better manage what they measure.

Integrated thinking is a decision making and an analysis process in which all corporate stakeholders participate as all stakeholders are affected by a company’s decisions and these interlocking causes and effects need to be considered and reported upon as an integrated whole.

Integrated Reporting seeks to communicate to stakeholders a business’ value creation model, performance, and potential together with an explanation of its effective and responsible utilization of all kinds of resources (Capitals). An Integrated Report shows why an organization exist (Purpose), how it achieves its purpose (Strategy, Business Model), and what the final results of its operations are, including the outputs (directly visible results like products, employment, profits, emissions, etc.) and outcomes (including the indirect material impacts created by the operations that may become visible over time). Therefore, an Integrated Report provides information not only on last year’s financial results and financial position of the institution, but also provides relevant information about the opportunities and the risks for long-term existence of the organization, its stakeholders, and the environment.

It is critical for corporations to be able to communicate their value proposition not just to the market and shareholders but also to other stakeholders like employees, customers, suppliers and society at large. As it becomes apparent that a significant portion of value creation is taking place from difficult to account for intangibles or ethical ESG conduct, the role of measuring and reporting becomes crucial. Leaders of tomorrow will be those executives and companies who are able to transcend todays financial numbers and explain the value proposition of their activities to all of their stakeholders in a manner which not only holds them accountable but also gives comfort to stakeholders on the positive outcome of their actions; this, in turn, will merit a long lasting, higher market valuation.

Thanks to Paul Chan for subject matter insight, to Mohan Kumar Prabhu & Gamze Talay for research and design support.

References

[1] Intellectual capital and social capital are critical elements of intangibles. Since its founding in 1991, ARGE Consulting has adopted a policy of utilizing one-day-a-week for nonprofit work to help develop the communities she works with as a way of developing social capital and one-month-a-year developing content and providing continuous education opportunities to its employees as an investment in human capital. This focus on intellectual and social capital is the key reason why ARGE has become a globally recognized Turkish management consulting firm.

[2] https://aicd.companydirectors.com.au/membership/company-director-magazine/2018-back-editions/november/intangible-assets

[3] https://storage.unitedwebnetwork.com/files/484/496ba7f2f5fb16896ece24813c3b82c4.pdf

[4] https://brandfinance.com/images/upload/gift_2.pdf

This article was first published by Argüden Governance Academy.