“Trust is the essence of good governance and the foundation for sustainable development.”

Trust is very fragile. It takes special attention to detail to build and even more to protect it.

As Warren Buffet says “It takes years to build a reputation and seconds to ruin it.”

In August 2019, we have witnessed a tectonic shift in the understanding of key business

leaders about the purpose of the corporation from ‘Business of business is business’1

towards ‘Doing good is good business.’ The CEOs from 181 of the world’s largest companies

— as part of The Business Roundtable — declared that the purpose of a corporation is not

just to serve shareholders, but “to create value for all our stakeholders.” This was a critical

milestone for business world to earn the trust of stakeholders.

Obviously, such a change did not happen overnight and examples of such a shift range from

Unilever’s former CEO Paul Polman who told his shareholders that he would manage the

company for the long term over a decade ago; Former Chairman of Royal Dutch/Shell, Sir

Mark Moody-Stuart who was instrumental in bringing anti-corruption among the ten

principles of UN Global Compact and who published ‘Responsible Leadership’; Chairman

Emeritus of the Global Reporting Initiative (GRI) and International Integrated Reporting

Council (IIRC), Mervyn E. King who promotes integrated thinking to ensure that companies

report not only their financials but material impacts on positive and negative ‘externalities’;

and also CEO of Blackrock, Larry Fink who asks companies to focus on purpose and

contributions to society to bring long term value appreciation.

There is a strong link between a focus on long-term value creation and building trust.

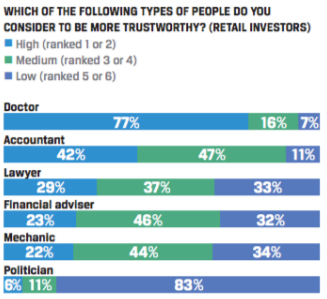

Unfortunately, when it comes to financial services sector trust has been fleeting. Financial

service professionals have often struggled to earn the trust of their stakeholders. According

to a survey in the CFAI 2020 Trust Report, doctors, for example, are trusted three times as

much when compared to financial advisers – who rate on a par with mechanics, but worse

than lawyers.

1 First formulated in 1970 by Milton Friedman at his New York Times article.

TRUST IS THE ESSENCE OF GOOD GOVERNANCE

Every institution that needs to mobilize other’s resources to achieve its goals needs to earn

the trust of its stakeholders. Transparency in relationships is the key to earning that trust.

Success requires effective utilization of resources entrusted to an institution. Being fair and

accountable to all the stakeholders whose resources are entrusted to the institution is the

key to sustainability of access to those resources. The communication and behavior of each

institution influences not only how its own resources are utilized, but also those of its

stakeholders. Therefore, consistency of the policies of an institution is key to ensure that

right expectations are formed throughout the value chain, thereby making the whole value

chain stronger. Risk is the kin of profit. Value creation requires measured risk taking.

Therefore, taking initiative and responsibility, which naturally involves risk taking is a key

element of value creation. Sustainability of success requires continuous improvement and

innovation. This in turn requires learning and the participation and involvement of all in the

organization. Hence, creation of a climate, which emphasizes good governance principles

and deployment of a good corporate governance culture is the key for sustainability 2.

Good governance is key for the financial industry not only for its own institutions, but also

for where the industry deploys the funds it manages. Generally, governance regulations are

tightened after major financial failures, when trust plummets.

WHY IS TRUST SHORT-LIVED IN SPITE OF BEING CORE TO FINANCE?

We all know that funds are aplenty. In that case why do investments rarely end up in places

where they could really make a difference and instead often gravitate towards old tested

solutions? Did asset management industry forget to focus on what is really important,

which is outcomes for the society? If the financial sector’s performance these days is being

defined by comparing itself to benchmarks, why do we then pay a lot of fees to asset

managers when all what they do is to crunch data?

2 CRAFTED principles for governance, as explained in Y. Argüden, “Boardroom Secrets: Corporate Governance

for Quality of Life”, Palgrave MacMillan (2009)

Individuals often fail to invest and dis-intermediate money because they believe the

financial system is not delivering on promises or changing fast enough to meet new

expectations. Challenge in the intermediation mechanism is that there is plenty of money in

the world, but it is being managed sub-optimally. For example, funds gravitate towards old

tried and tested solutions, even when they are not satisfying new expectations or

generating returns commensurate to requirements. In spite of growing pools of capital, the

status quo remains the same.

Additionally, throughout history, economic crises have been associated with market

failures. From a public point of view, the people who benefitted from an economic crisis

were the financials professionals who initiated them, they were also the ones, who took

advantage of the crisis and became the recipients of public funds in terms of government

bailouts. Consequently, people link crises to the failure of financial professionals in taking

appropriate actions, the most recent being the 2008/2009 global financial meltdown, after

which trust in banks eroded significantly.

Finance is often based around asymmetric relationships where one party possesses

significantly more information than the other – for example an investment advisor and his

client who is not well informed. The essence of professionalism is putting your client’s

interests before your own as you have a duty of care towards your clients. In such

circumstances, trust is always essential, as in doctor-patient or attorney-client

relationships. The problem is that sometimes financial advisors or intermediaries may call

themselves ‘professionals’ but they may put their own pecuniary interests above the clients’

goals. Trust is absolutely core to finance.

SUSTAINABILITY IS BECOMING A HIGH PRIORTY FOR INVESTORS

As financial professionals struggle with trust issues, there are new emerging developments

happening. These days, various stakeholders in the society are also raising their concerns

about the fact that the world we live in is running out of resources, externalities are

becoming unmanageable and thus, causing detrimental climate change. Countries,

governments, global exchanges, regulators, corporations are responding to those pressures

by balancing local needs with global pulls.

Accordingly, there is also increasing responsibility of investors for stewardship of

sustainable action. Asset managers these days are expected to exercise higher oversight on

ESG matters as more of them sign up to investment practices laid down by the UN to reach

Sustainable Development Goals (SDGs) in the future. Adequate oversight on ESG could help

managers improve on the trust deficit brought about by information asymmetry implicit in

financial market intermediation.

For some asset managers, ESG is not a new burden in first place. Responsible asset

managers have been integrating ESG concepts into their core process for years. The process

of trying to figure out if the governance of the corporation is working properly or how a

corporation is treating its customers and suppliers has been a common part of investment

due diligence. The E, S, G acronyms are now giving visibility to parts of the processes that

have been part of similar concepts being used for a long time.

CHALLENGED BY AN INABILITY TO DEFINE A CLEAR SOCIAL PURPOSE

For trust to exist it needs to be encouraged and cultivated with a clear social purpose.

However, unlike for asset owners, it is very difficult for asset managers to commit to a single

statement of purpose. Asset managers have a fiduciary duty to their investors and a

mandate to abide by. For example, in the United States it is written in law that asset

managers’ fiduciary duty is to primarily focus on financial return while there is no written

law to ensure ESG integration into investment decisions. Then, there are different legal

approaches to fiduciary duty in other regions. For example, in France there is Article 173,

which makes ESG integration a requirement by law. Similar laws also apply in the UK, as

well as in the rest of the European Union. Therefore, an ability to define a social purpose to

start with may depend on where you sit. And many a times there may be difficulties in how

to incorporate externalities into the investment decisions.

The good news is that this is improving. Even in the United States, one of the most litigious

places from the fiduciary duty perspective, impetus to consider ESG in investment decisions is

increasing. According to the Conference Board3

, recently the notion of fiduciary duty is

expanding to include sustainability issues. Increasingly the pursuit of sustainable business

initiatives is viewed as consistent with corporate governance standards. In particular, judicial

action4

, recent stakeholder constituency statutes5

, and statutory exculpatory provisions under

corporate law6 have laid the groundwork for boards to consider non-shareholder interests and

concerns in making investment decisions7

. According to Mr. David Atkin, CEO of CBUS, a large

pension fund in Australia fiduciary duty in Australia is also shifting. Mr. Atkin says that these

days it is less about what you can’t do as, increasingly, regulatory and beneficiary pressures are

requiring investors to demonstrate how they take account of climate considerations and social

issues. Additionally, he explains that fiduciaries that haven’t been seen to take account of these

issues or sufficiently demonstrate the assessment of ESG, are exposing themselves to reputational

and litigation risk. “ESG integration is about having a holistic process for assessing risk and for

recognizing the outcomes our investments can have on the society in which our beneficiaries will

retire”.

EARNING TRUST WHILE DEPENDING ON INCONSISTENT DATA

Consistency in behavior, in actions, or in delivering continuous results is a sign of good

leadership and fostering trust. However, one of the major difficulties asset managers are

admitting is the unreliability and inconsistency of data, which they rely on for delivering

results.

3 The Conference Board, “Sustainability in the Boardroom,” DN-008, June 2010

4 See, for examples of cases where the legal courts underscored the importance of assessing the impact on key

stakeholder relations of a Business decision made in the context of hostile takeovers a shareholder instituted

derivative actions: Unocal Corp. Mesa Petroleum Co., 493 A. 2d 946, 955 (Del. 1985), discussing how boards

should consider the impact on constituencies other than shareholder when analyzing the reasonableness of

defensive measures; and Paramount Communications, Inc. v. Time Inc., 571 A. 2d 1140, 1153 (Del. 1989)

5 For example, 15 Pa. Cons. Stat. §1715. In general, see Kathleen Hale, “Corporate Law and Stakeholders: Moving

beyond Stakeholder Statutes,” Arizona Law Review, Vol. 45, 2003, p. 829

6 Delaware Code Annotated, Title 8, Section 102(b) (7), permitting the use of clauses in the certificate of

incorporation (therefore approved by shareholders) to insulate corporate directors from monetary liability for

any action arising from a breach of their duty of care. Exculpatory clauses provide more freedom and leniency to

directors in their decision-making capacity and encourage them to take strategic risk.

7 Pursuit of Social Investments,” The Conference Board, Director Notes No. DN-002, January 2010.

There are non-profit and independent standards organizations, such as GRI, SASB, TCFD,

which are aiding this process and offering guidance both to asset managers as well

corporations with the goal to improve the quality of data; as well as voluntary initiatives

such as UN Global Compact and International Integrated Reporting Council that provide

principles rather than standards.

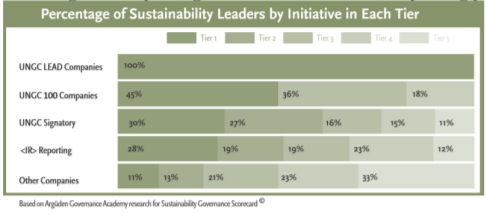

Sustainability Governance Scorecard, an impact research conducted by Argüden

Governance Academy, aims to improve transparency of meaningful disclosure. It

encourages peer learning by promoting best practice examples selected from sustainability

reports by Global Sustainability Leaders from seven countries across 10 sectors. 8 The

study also shows that corporations who voluntarily adopt UN Global Compact principles

and Integrated Reporting tend to have better ESG reporting performance.

The main problem here is that despite emerging standards, the corporations across the

globe are still largely reporting ESG data on a discretionary basis. This causes many data

discrepancies. For example, one corporation may report sustainability data only for the

home country, while another corporation may cover all regions it is operating in. Or one

corporation may have its non-financial data partially/fully audited, while the other

corporation may not have any assurance at all9.

Even though it is correct that data is crucial for asset managers, its absence should not

become an excuse for inactivity. If we have data, then in theory machines could be doing the

job of asset managers. Surely, the role of asset managers is to boldly go where the data is

poor and to exercise judgment on the likely future direction of finance. Maybe the financial

services industry is being too conservative and unwilling to innovate. This could be another

reason why trust in active asset management skills has been so low. Then the question

comes up: why should clients pay asset managers a lot of fees if all what asset managers

primarily do is to crunch data?

In order to resolve the issues related to data inconsistency, asset managers could propose

that data should be more focused on outcome rather than on just comparability. Maybe

asset managers could use UN SDGs as the common goalpost and try to quantify the impact

on SDGs. Maybe asset managers need to go beyond past mistakes. Over the last generation

asset management became an industry defining performance based on a comparing itself to

benchmarks, rather than focusing on outcomes for the society. Ironically, the

8 https://sgscorecard.argudenacademy.org/

9 https://sgscorecard.argudenacademy.org/

incompleteness of ESG data could now provide a great reason to focus on what is really

important which is the ultimate outcome, rather than comparability to predefined bogeys.

TRUSTWORTHINESS MAY DEPEND ON WHERE YOU SIT

An investor’s ability to have a genuine influence and earn trust may depend where

operations are physically located. ESG looks very different depending upon where you sit…

For example, many emerging markets still rely on extractive industries for growth. Brazil

may depend on rainforests whereas South Africa may depend on coal mining and depending

on livelihood issues one’s perception of ESG may change. Also, some countries may be more

incentivized compared to others when it comes to ESG integration. Their governments,

exchanges or regulatory agencies may be responding more decisively to threats from

climate change or externalities.

- Switzerland, Hong Kong and Singapore that have historically functioned as financial

hubs may have an inherent incentive to take leadership and push for ESG

integration as they may wish to be first movers in an increasingly ESG driven

environment. EU members such as Germany and France operating under the

influence of the European Finance Commission as well as places like Mainland China

in Asia are locations where climate action is something that is being pushed by

governments and regulators to ensure delivery on international commitments. In

the process, they may be creating a foundation for ESG integration. - Areas where ESG integration is taken seriously, such as in the UK, Northern Europe,

and South Africa, there is a sophisticated audience for sustainability. The bottom up

demand from society is simply higher in these regions, which incentivize regulatory

agencies to take action faster. Mandatory regulation also seems to experience fewer

backlashes from corporations in jurisdictions where the cultural sensitivities are

higher. - Then there are countries like United States, Japan, South Africa, Brazil, Hong Kong,

Turkey, India, Thailand and Colombia that may simultaneously have large

government pension funds or influential exchanges that have pushed for ESG

integration through issuing indices and increasing flow of funds into the space.

Examples are sustainability indices such as Nasdaq Clean Edge US Index, OMX GES

Ethical indexes, OMX CRD Global Sustainability Index offered by Nasdaq; three ESG

indices for Japanese equities launched by Japan’s GPIF (Government Pension

Investment Fund), the creation of FTSE/JSE Responsible Investment index by JSE

(Johannesburg Stock Exchange), the evolution of ISE Corporate Sustainability Index

by B3 (Bolsa do Brasil), the design of Hang Seng Corporate Sustainability Index by

HKEX (Hong Kong Stock Exchange), the foundation of BIST Sustainability Index

created by Borsa Istanbul and the formation of Nifty100 ESG Index by National

Stock Exchange of India (NSE). The Thai Government Pension Fund (GPF) has also

been spearheading sustainable investing among Thai asset managers. GPF

contributed by initiating a collaborative engagement among Thai asset management

firms to promote good governance and ESG practices among corporates. BVC

(Colombia Securities Exchange) pushes for ESG integration through its prestigious

Investor Relations committed program, where they utilize a dedicated set of ESG

questions to engage listed corporations on a regular basis. In spite of not being

compulsory, many large corporations listed on BVC aspire to be part of it because of

its reputation. It is naïve to think that ESG can be promoted by private action alone.

It needs support from asset owners, global exchanges and regulatory agencies

acting in tandem to give it momentum. Therefore, global exchanges are creating

enablers for asset managers through indices and other initiatives to evaluate ESG

fund returns and create awareness about the sustainability performance of most

liquid companies on their exchanges. Additionally, global exchanges actively

promote sustainable investing among investment practitioners and various

stakeholders through seminars and training activities. Nasdaq’s “ESG Product

Workshop”, JSE’s “ESG Investor Showcase”, Borsa Istanbul’s “BIST Sustainability

Platform”, NSE’s “Stakeholder Roundtables” and SET’s “ESG Education for Thai

Capital Market Professionals” are great examples of enabling events designed by

exchanges to encourage engagement and collaboration amongst asset managers,

corporations and NGO’s. As mentioned before, there is a difference between asset

managers and asset owners. Intermediaries do not have full agency power.

However, asset owners and regulatory agencies have the power to move the asset

managers towards better ESG integration. - Lastly, there are global regions where inaction by regulatory agencies has not

stopped asset managers from taking the lead in ESG’s financial education. Some

investors in countries such as United States, Canada and Australia became global

leaders forcing corporations to make more disclosures. Stakeholder relations seem

to be in front and center for ESG integration in these countries. As data is not easily

accessible in standard formats, engagement with corporations is key. Therefore,

many initiatives are being taken by asset managers themselves to establish proper

communication with corporations and improve the quality of data.

LOOKING INTO THE FUTURE

There are several ways asset managers can act which can ensure that going forward they

earn trust from clients who are increasingly concerned about sustainability issues. ESG may

provide an opportunity for differentiation and also help build stronger relationships with

the clients and stakeholders. The line of trust asset managers failed to build for years could

reverse course now in a new world that is changing rapidly in many ways, given the

devastation caused by the impact of Covid 19. Maybe now it is a perfect time for asset

managers to make a difference by ensuring that funds are flowing to places where they will

help find a solution to dire challenges faced by humanity, whether that be climate change or

one produced by the pandemic. Trust in financial services could develop faster if the

industry changed fast enough and funds went to areas which many conscious investors

would consider as responsible, meeting the needs of a sustainable future.

Long-term holistic thinking will assist asset managers in identifying sustainable value and

in avoiding value traps. Paying attention to ESG is not only good for risk management, but

also a lead indicator for future value creation.

In the future, we need to see more evidence that ESG considerations are becoming part of

the values and beliefs by ALL asset managers. While some asset managers immediately

became torchbearers as the new ESG principles were introduced, it has been somewhat

disappointing to find out that others still do not fundamentally believe in ESG. Some asset

managers to this date do not have deep seated views about sustainability enshrined in their

own mission and vision statements. ESG faces a challenge of getting stuck in a tug of war

between believers and non-believers as it is pushed as a concept—one that needs to be

embraced instead of a concept whose outcome is directly measurable in terms of its impact.

This needs to change.

In conclusion, trust cannot exist without creation of value, and value creation without trust

is unsustainable.10 Asset managers need to adapt to a rapidly changing world with longterm integrated thinking or need to face a long-term decline in their prospects going

forward.

10 https://trust.cfainstitute.org/wp-content/uploads/2020/05/CFAI_TrustReport2020_FINAL.pdf

This article was first published by Argüden Governance Academy.