There are different ways an organization can attract and engage its various stakeholders. Having an inspiring purpose articulated in form of a mission statement may be one of the most effective ways. An even simpler concept is presented by Simon Sinek, the British-American author, who offers “WHY” as an influential notion in his impactful book “Start with why”.

When trying to sell their goods and services, organizations often guide their customers on value propositions using clever marketing strategies on pricing and promotions. However, using marketing subterfuge in order to draw customers to make a purchase usually ends up only achieving short term gains. On the other hand, sustainable sales and long-term growth is often enabled when an organization is truly capable of inspiring trust in its customers and stakeholders to the extent that they look up to the organization to define their needs and solutions for the same. Therefore, Simon Sinek makes the following argument in his book: “Organizational leaders need to understand why, how and what the entity does in the business environment. They need to establish the needs, wants and expectations of their stakeholders.”

Asset managers are the same. Just like in any other business, asset managers also need to be able to articulate their “why” clearly when they are offering their services. They not only have to deliver on performance, but also need to figure out how they can inspire their clients to entrust their life savings with them. This is responsibility, more so given the asymmetric nature of information available to an asset manager over what his or her client has access to. Accordingly, there are plenty of possible mission statements an asset manager may articulate – the concept of Environment, Social and Governance investing (ESG) is one, and we believe offers the most opportunity for leadership and the ability to resonate with clients and thereby build a bond of trust.

Unlike many corporations, asset managers find it exceedingly difficult to commit to a single statement of purpose because of certain contradictions. For instance, it is easy for asset managers to focus on fiduciary duty and hide behind mandates which they have to abide by, instead of looking to define their mission statement built on a set of shared sustainability values. Regulators also do not make it easy. For example, in the United States it is written in law that asset managers’ fiduciary duty is to primarily focus on financial return, while there is no written law to ensure ESG integration into investment decisions.

Asset management firms manage funds for individuals and institutions by making investment decisions on their behalf with an objective of delivering returns. At the same time, they consider their clients’ unique circumstances, risk appetite and preferences. Historically, discerning managers used to integrate ESG issues into their risk management practices to ensure the sustainability of their investment processes. As ESG issues are becoming mainstream, the challenge they face now is to move it from an internal process to a mission statement which helps stakeholders understand the purpose, the “Why” of their goals.

One of the best ways to understand asset managers’ dilemma is if we put ourselves in a similar personal situation. As individuals, there are times when we find difficult to articulate our “why” to others in spite of having formulated a clear purpose in our own minds. The reason is because delivering on a purpose is easier than receiving endorsement and buy-in from other parties. Acceptance from others requires leadership skills to convert ideals into actionable goals.

Unlike many other industries, the asset management industry operates in an eco-system where they not only have to satisfy customer expectations, but also operate within boundaries defined by regulators. Consequently, any change requires leadership and an ability to convincingly articulate ideas to multiple stakeholders. Also, asset managers may have to balance the expectations of their shareholders, who may view ESG investments as exclusionary and limiting to organizational growth.

The good news is that all parties are increasingly recognizing the need for ESG primacy, though the inability to arrive at a common template is creating dissonance, which requires further leadership for bridgebuilding.

The industry needs to step forward. Otherwise, they will have to live with consequences of templates which are defined by stakeholders whose understanding of their needs may be limited and many a times overwhelmed by extraneous circumstances.

Regulatory Momentum may Help Asset Managers to Express Their “Why”

Asset managers can play an active role in having an impact on ESG issues. As fiduciary owners of companies they invest in, they can help shape management decisions and thereby the final outcome. Regulatory agencies as well as global stock exchanges are considered key stakeholders. Exchanges are capable of creating standards to ensure there is trust in the system and fill the gap between investors and other market participants. These initiatives – when handled correctly – lead to better and fair investment decisions. Funds are consequently allowed to flow where they could make a difference.

Regulatory Challenges

One of the challenges asset managers face is the fact that regulations and practices are developing in isolation from each other and not based on an adequate understanding of investment practice. ESG policies must move away from the assumption that the impact of an investment strategy is the same as the characteristics of the underlying portfolio. Instead they should support and develop the full range of tools investors have available to influence real-economy outcomes, including capital allocation, stewardship and real-economy policy engagement.1

In their current form, ESG policies seem to be lacking two core elements: first, a universal consensus on what constitutes an ESG investment and a way for asset managers to assess ESG compliance in their portfolio; and second, reporting on ESG in a consistent framework, which is comparable and helps measures impact.

Global bodies like the UN Principles for Responsible Investment (UN-PRI) have helped develop the European Union taxonomy. They are aware of the challenges and urge investors to support the drive towards a common sustainability taxonomy. One of the main goals is to prevent green-washing. It is not just about the carbon saved, or the waste diverted from a landfill, but whether the economic activities we finance are consistent with the future environmental state to which society and governments are committed.2

The challenge towards coming to a common ground was highlighted in a Morningstar study ‘The Evolving Approaches to Regulating ESG Investing’. This research showed the contrast between global regions. In the US, where climate change is a “contested concept”, ESG investment factors must be justified by explaining “why,” while in Europe, investment managers must explain “why not”.

Even the EU, which is a leader in ESG initiatives, is struggling to come up with common standards. The Technical Expert Groups (TEGs) on sustainable finance set up in 2018, published reporting guidelines in 2019, but they only provide non-binding advice for disclosing climate change mitigation investments and activities. In order to express their frustration with a lack of consensus on climate change, 631 institutional investors with more than $ 37 trillion in assets organized the largest ever joint call on climate change during the 2019 COP 25 in Madrid. These investors wrote and signed a petition reiterating their full support for the Paris agreement. They urged all governments to implement the actions that are needed to achieve the goals of the Agreement, with the utmost urgency.

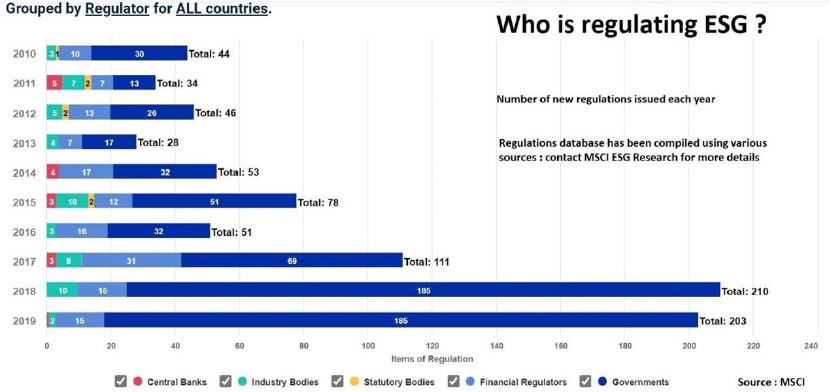

MSCI in a recent study found that increasingly governments around the world are becoming more active and writing new guidelines and regulations at a rapid pace to ensure the industry is delivering on ESG commitments (as shown in the chart below). In an environment where common templates are still being debated, the industry needs to step forward to frame a common ground. Otherwise, very soon it will have to live with the consequences of having to work with diverging guidelines issued by different regulators who are responding to different pressures in their respective home countries.

Some regulatory convergence is happening in spite of a Trans-Atlantic divide

Concerns for ESG issues is global but practices and priorities vary around the world. This is the biggest challenge that the asset management industry has to deal with especially as many investing mandates are more global in their outlook than regulators who are locally driven.

On a positive note, there is some regulatory convergence happening on how to approach ESG in mandates and fiduciary duties in spite of a still existing Trans-Atlantic divide.

Europe represents almost half of the current $30.7 trillion of investable assets in sustainability funds, according to the Global Sustainable Investment Alliance. The rise of eco-political parties in power in Europe, millennials and ‘green’ investors have compelled a wave of responsiveness.

Awareness is also growing among investors and companies in the United States. Despite the fact that there is no consensus on ESG regulation on a federal level, some states in the U.S. like California and Illinois are taking the lead in promoting sustainable investing and setting standards via asset managers such as CalPERS and CalSTRS.

California has historically served as a pioneer for ESG integration in the management of its pension systems and developing frameworks. This includes CalSTRS 21 Risk Factors, which have served as a guide for other state pension funds for incorporating ESG considerations. Additionally, Illinois later signed the Sustainable Investing Act into law, signaling the next step in state ESG integration requirements. Illinois’ new law, effective January 2020, requires all public or government agencies that manage public funds to implement responsible investment policies covering all public funds under their control.3

Client Momentum may Help Asset Manager Express Their “Why”

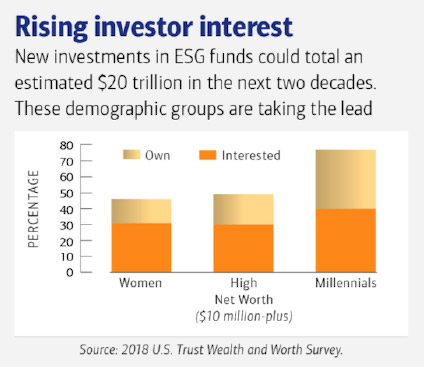

Client driven trends could propel asset managers in articulating their purpose. First of all, there is an anticipation that the pool of wealth in the hands of ESG conscious millennials will grow faster than the amount available in the hands of older generation asset owners who have been less sustainability driven. Secondly, a pandemic that has upended our lives is highlighting the value of ESG investments as the ensuing health crisis has reminded society of the dangers of ignoring expert advice on sustainability.

Wealth of Transfer: Millennial Investors vs Investors aged over 60

According to Capgemini’s World Wealth Report 2020, more than a quarter (27%) of high net worth individuals— those with investible assets of $1 million or more — said they were interested in sustainable products. More than two-fifths (41%) of high net worth individuals aged under 40 were drawn to sustainable investments compared with just 16% of those aged over 60, Capgemini’s report found.

With millennials now accounting for the new wealth generation — and many more estimated to become beneficiaries of the so-called “Great Wealth Transfer” as baby boomers pass on their possessions to their heirs —more sustainable investments are predicted. It’s estimated that 45 million U.S. households will transfer $68 trillion in wealth over the next 25 years, according to a report from financial services research firm Cerulli Associates.

Covid 19 & ESG-compliant companies outperforming in a major crisis

JPMorgan said that the pandemic could prove to be a “major turning point for ESG.” Its survey of investors with combined assets of more than $13 trillion found that 71% of investors thought Covid-19 could increase awareness for risks such as climate change and biodiversity losses.4

In another study, HSBC analyzed 140 stocks with highest ESG scores above the global average. To evaluate Covid19 impact, it looked at performance from 10th December 2019, the onset of the crisis, to 23th March. The ESG shares beat others by approximately 7%.5

An explanation for these results is quite obvious. A key part of environmental, social and governance is to look at how companies serve society, and what this may mean for the future. When a crisis like COVID-19 rears its face investors can appreciate the defensive quality of ESG with its emphasis on stronger governance. Companies which have pre-established monitoring systems for the well-being of their employees and customers can quickly adapt to a major crisis.

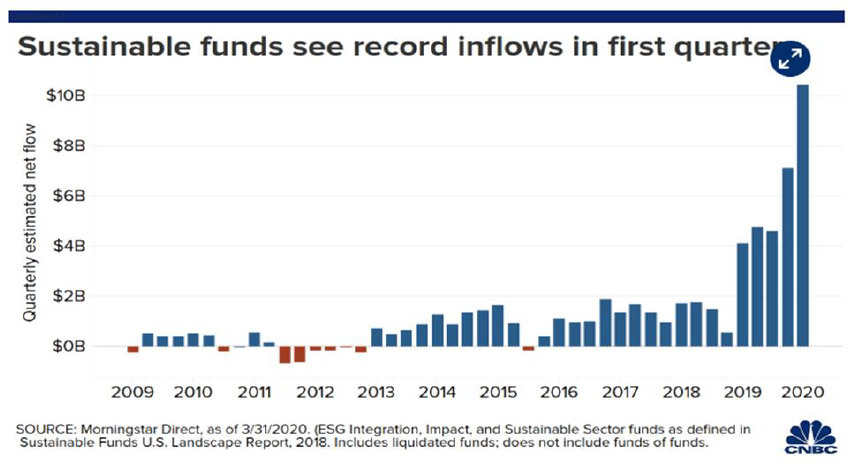

No wonder investors are putting more of their money into funds which are classified as sustainable, as seen from the chart above. This is a trend which is incipient and something that managers can no longer ignore as a fad.

Client Education is essential

ESG objectives may be simple, but their implementation through investment funds can be complex in terms of impact and performance measurement. There is a need to use a longer-term horizon than would be the norm for traditional products. Therefore, client handholding and education may be required to ensure that they stay the course.

A 2019 Natixis global survey revealed that 75% of individual investors worldwide say it’s important to align their investments with their personal values and ethics. About 50% say they do just that, but the other half say they lack the information needed to choose those investments. An even greater percentage of financial advisors — 68% globally — say they would be more likely to recommend ESG products to clients if there were better data and reporting on these investments, while 71% of U.S. advisors worry that investments labeled “green” are not genuinely sustainable investments.6

This clearly shows that the market demand exists but the ability to satisfy it requires all stakeholders to come together and help deliver on a common taxonomy so that the dissonance between client expectations, regulatory mandates and what asset managers can deliver is narrowed.

Recent Collective Action by Regulatory Agencies and Exchanges

Inspired by lessons learned from the Covid-19 crisis, the London Stock Exchange has started a new collective climate change action in collaboration with SSE (United Nations Sustainable Stock Exchanges Initiative) and supported by CalPERS. This partnership intends to engage other global exchanges. It will be a coalition working to improve the environmental data reported by global companies trading on these exchanges.7

On another note, the Monetary Authority of Singapore (MAS) just issued a consultation paper on handling of “Environmental” issues by asset management industry. It is looking to ensure that asset managers: (a) incorporate environmental issues in their risk management processes, (b) have a robust capacity building to ensure that their organizations over time incorporate these principles and lastly (c) as part of their stewardship responsibility engage with investee companies on environmental issues.

Additionally, Nasdaq recently lead by example by announcing an immediate action plan to better deal with social issues. The statement was also meant as a response to recently highlighted social issues in the U.S. where the health crisis has been turning into a crisis of confidence and trust. Nasdaq is setting up a multi-dimensional approach that would grow the company’s diversity and inclusion. This will include larger investments in human resources as well as a promise to release a new workforce diversity metrics.8

The Colombia Securities Exchange has also been engaged in separate ESG initiatives within July of 2020: (a) launch of their sustainability guidance, (b) a three-day virtual event organized together with GRI and PRI to engage financial institutions, insurers as well as government representatives and finally (c) announcement of their commitment to task force for responsible investment which is a dialogue between public and private actors to promote responsible investing in Colombia.

B3 (Bolsa do Brasil) recently got approved a new ESG Strategic Plan by its Sustainability Committee. In the context of this plan, a climate strategy has also been created. The ambition in the climate agenda is to be a hub on the theme in Brazil, connecting customers, market players and specialized partners to develop the market, strengthen their existing climate products portfolio (ISE, ICO2, Green Bonds) and opening new business fronts, such as “Carbon Market” and “Impact Business”.

More of these initiatives are needed to be designed and promoted by regulatory agencies, global exchanges, corporations, investors and even individuals. According to an impact research called “Sustainability Governance Scorecard” by Argüden Governance Academy, which evaluates companies through a governance lens, only 35% of leading ESG-compliant global corporations align their overall strategy with SDG 17 (Partnership for Goals.) The study therefore highlights an urgent need for many more collective action plans.9

According to Rajesh Chhabara, managing director of CSRWorks International, a Board-level buy-in is still a big missing piece and delays acceptance from various stakeholders. “There is an urgent need to rampup the Boardroom competence in sustainability. Directors should be required to complete regular training to build the necessary sustainability skills and knowledge. ESG should also be made part of the directors’ fiduciary duty.”

Indeed, when personally invested and sincerely involved, board members could become an organization’s most thorough supporters and strategists. Then it would be likewise easier to bring to life such collective initiatives leading to stronger contribution to SDG17.

In Conclusion

Asset management is at cross-roads, a time where circumstances are leading to rapid adoption of ESG as a mainstream concept. Yet, as an industry it is torn between conflicting pressures and responsibilities, and thus requires leadership to find a collective common ground.

Asset management industry needs to come forward before it is too late. Without proper leadership, it will face the difficult challenge of having to live with rules defined by a varied set of stakeholders working to deliver on their own narrow set of goals. And those goals can consequently be at cross purpose with the ultimate purpose of delivering a better future for humanity today.

References

[1] https://esgclarity.com/a-generational-opportunity-pri-issues-recommendations-for-renewed-sustainable-finance-strategy/

[2] https://www.ipe.com/how-the-eus-sustainability-taxonomy-will-work-for-investors/10031623.article

[3] https://malk.com/the-rise-of-esg-regulation/

[4] https://www.jpmorgan.com/global/research/covid-19-esg-investing

[5] https://www.gbm.hsbc.com/insights/global-research/esg-stocks-did-best-in-corona-slump

[6] https://www.thinkadvisor.com/2019/06/27/esg-data-is-missing-link/

[7] https://sseinitiative.org/all-news/sse-launches-climate-disclosure-work-with-mark-carney-and-lseg/

[8] https://www.nasdaq.com/articles/adena-friedman-believes-now-is-the-time-to-build-a-more-inclusive-economy-2020-06-19

[9] https://sgscorecard.argudenacademy.org/

This article was first published by Argüden Governance Academy.